Quick summary: The global tire industry is a multi-billion-dollar powerhouse. As we enter 2026, the landscape of the Top 10 Global Rubber Tire Exporters is shifting. From Chinese scale to German precision, discover which nations lead the market, how EV trends influence trade, and how strict sustainability mandates are now redefining the future of global supply chains.

The Top 10 Global Rubber Tire Exporters play a critical role in powering the global automotive industry, supplying passenger vehicles, commercial fleets, industrial machinery, and emerging EV markets across continents. As international trade continues to shape automotive supply chains, understanding which countries dominate tire exports and why has become essential for importers, OEM procurement teams, distributors, and investors.

The global tire export market is valued at tens of billions of dollars annually, with a significant share concentrated among a handful of leading manufacturing nations. These exporters influence pricing trends, supply chain resilience, sustainability standards, and regional trade dynamics. From high-volume production hubs in Asia to premium engineering centres in Europe and North America, the competitive landscape reflects a mix of scale, innovation, raw material access, and trade strategy.

Between 2024 and 2026, tire export growth has been driven by rising vehicle demand, expansion of commercial transport fleets, increased replacement cycles, and accelerating EV adoption. At the same time, regulatory pressures around sustainability, deforestation-free rubber sourcing, and carbon emissions are reshaping global trade flows.

In this blog, we break down the Top 10 Global Rubber Tire Exporters, analyze their market share, examine trade data trends, and explore what these rankings mean for global buyers and supply chain decision-makers navigating an increasingly competitive and regulated marketplace.

The global rubber tire industry is one of the most critical segments of the automotive value chain, supporting passenger vehicles, commercial transport fleets, agriculture, aviation, mining, and industrial machinery worldwide. Valued at hundreds of billions of dollars annually, the tire market is highly export-driven, with international trade accounting for a substantial share of total production. Very few countries are self-sufficient in tire manufacturing, making global exporters essential to vehicle production, aftermarket distribution, and fleet maintenance across continents.

Exports play a central role in maintaining supply chain continuity for automotive OEMs, distributors, and retailers. Tire manufacturers often produce at scale in cost-competitive regions and ship globally to serve diverse markets. As a result, trade flows influence pricing, availability, freight demand, tariff exposure, and sourcing strategies. For procurement teams and global distributors, understanding which countries dominate tire exports is not just informational it directly impacts supplier diversification, risk management, and long-term purchasing decisions.

Global rubber tire exports totaled $99.8 billion in 2024 (new tires, +0.7% YoY from $99.1B 2023, +40.8% from 2020), with volume ~1.1B units amid Asia-Pacific dominance (50.4% share, $50.3B). China leads at $22.2B (22.3%), Thailand $7.4B (7.4%), Germany $5.8B (5.8%), Japan $5.2B, USA $4.9B; top 15 hold 74.7%. EV tires (+20% demand) and aftermarket drive growth (market $172.4B 2025 to $237.1B 2034, CAGR 3.36%); China tire exports 8.83M tonnes Jan-Nov 2025 (+3.7%), shifting to Middle East/Africa amid EU/US tariffs/EUDR traceability for natural rubber supply.

Demand dynamics are also evolving rapidly. The rise of electric vehicles (EVs) is driving innovation in low rolling resistance and high-durability tires. Expansion in commercial transportation and logistics fuelled by e-commerce growth is increasing demand for truck and bus radial tires. Meanwhile, the global aftermarket segment remains robust, as replacement cycles often exceed original equipment demand in many regions. Emerging markets are further contributing to export growth through rising vehicle ownership and infrastructure expansion.

Against this backdrop, exporter rankings offer valuable insight into industrial strength, production competitiveness, and global trade positioning. For buyers, they highlight stable sourcing hubs and emerging supply regions. For investors and trade analysts, they signal where manufacturing capacity is expanding and where competitive advantages are consolidating. In a market shaped by supply chain resilience, trade policies, sustainability requirements, and shifting consumer demand, understanding the top global rubber tire exporters provides strategic clarity in an increasingly complex automotive ecosystem.

China is the largest global exporter of rubber tires by value, followed by Thailand, Germany, Japan, and the United States. Asian manufacturers dominate global tire trade due to lower production costs, integrated rubber supply chains, and large-scale manufacturing infrastructure.

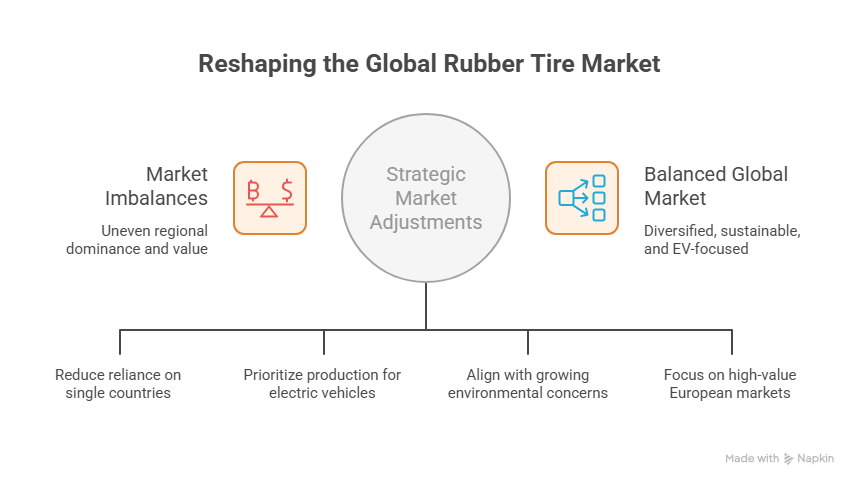

The 2026 global tire market is characterized by a continued shift toward Southeast Asian manufacturing hubs and China’s massive scaling of “green” and EV-specific tires. While European and American exporters maintain a stronghold on the high-end OEM (Original Equipment Manufacturer) segments, cost-efficiencies in the East are driving volume.

| Rank | Country | Estimated Export Value (USD) | Global Share | Key Strength |

| 1️⃣ | China | $22–25 Billion | ~25–28% | Unrivaled scale; leading the transition to budget-friendly EV tires. |

| 2️⃣ | Thailand | $9–11 Billion | ~10–12% | Natural rubber supply-chain integration; hub for Japanese & US brands. |

| 3️⃣ | Germany | $8–10 Billion | ~9–10% | Premium performance tires; dominant in luxury European OEM fitments. |

| 4️⃣ | Japan | $7–9 Billion | ~8–9% | Cutting-edge R&D; leader in high-durability and specialty innovation. |

| 5️⃣ | United States | $6–8 Billion | ~6–7% | High-margin specialty, agricultural, and premium off-road tires. |

| 6️⃣ | South Korea | $5–7 Billion | ~6% | Strong global branding (Hankook, Kumho) and tech-driven R&D. |

| 7️⃣ | India | $4–6 Billion | ~5% | Rapidly growing capacity in commercial and heavy-duty radial tires. |

| 8️⃣ | Vietnam | $3–5 Billion | ~4% | Rising manufacturing hub; beneficiary of global supply chain diversification. |

| 9️⃣ | Indonesia | $3–4 Billion | ~3–4% | Rich natural rubber resources; focus on two-wheeler and budget radials. |

| 🔟 | France | $2–3 Billion | ~2–3% | Global brand leadership (Michelin) and high-performance racing tires. |

China remains the world’s largest exporter of rubber tires by both value and volume.

Key Strengths:

China exports a broad portfolio:

Its dominance is supported by:

China’s share is particularly strong in price-sensitive markets.

Thailand benefits from being one of the world’s largest natural rubber producers.

Key Strengths:

Thailand has positioned itself as a reliable alternative sourcing hub amid global trade tensions.

Germany leads in high-value, premium tire exports.

Key Strengths:

German exporters focus less on volume and more on:

Germany plays a major role in European intra-regional tire trade.

Japan is known for advanced engineering and specialty tire segments.

Key Strengths:

Japanese exporters are particularly strong in:

The U.S. focuses heavily on high-value tire exports.

Key Strengths:

The U.S. also benefits from trade agreements that support exports within North America.

South Korea has become a major global exporter with strong global brands.

Key Strengths:

Korean manufacturers have aggressively expanded into:

India is emerging as a competitive exporter, particularly in commercial segments.

Key Strengths:

India’s export growth is supported by:

Vietnam has gained prominence as global production shifts diversify away from single-country dependency.

Key Strengths:

Vietnam is increasingly viewed as a strategic alternative sourcing base.

Indonesia leverages its strong natural rubber supply.

Key Strengths:

Exports are particularly strong in:

France’s exports are driven primarily by high-end global brands.

Key Strengths:

France competes on quality, brand value, and technological differentiation rather than export volume.

Global rubber tire exports have shown steady recovery and expansion following supply chain disruptions earlier in the decade. Between 2024 and 2026, export growth is being driven by:

Export value growth is outpacing volume growth in some regions due to:

Asian countries continue to dominate global export volumes, while European and North American exporters focus more on high-value premium segments.

Yes. Global tire exports are growing steadily due to rising vehicle demand, fleet expansion, and aftermarket replacement cycles, particularly in Asia and emerging markets.

The rise of electric vehicles (EVs) is reshaping tire export dynamics.

EVs require tires that offer:

This has led to:

Countries with advanced manufacturing and R&D ecosystems (e.g., Germany, Japan, South Korea, and China) are benefiting from this shift.

EV-specific tire exports are expected to grow faster than conventional tire segments between 2024 and 2026.

Sustainability is becoming a major trade driver in the tire industry.

Key export trends include:

Importing regions, particularly the EU, are increasing regulatory scrutiny around:

Exporters that can demonstrate traceable, sustainable rubber sourcing are gaining competitive advantage.

This trend is shifting trade flows toward manufacturers with strong ESG credentials and certified supply chains.

Trade policies continue to significantly influence tire export patterns.

Major influencing factors:

These measures have:

For example, when one major importer imposes tariffs on a specific exporting country, manufacturers often redirect supply to alternative markets.

Trade risk management is now a critical factor for global tire exporters and distributors.

Regional trade agreements are reshaping global tire trade flows.

Key influences include:

Examples of trade blocs influencing tire exports:

Manufacturers increasingly structure production networks to optimize tariff benefits and minimize trade barriers.

Between 2024 and 2026, tire export dynamics are being shaped by:

For importers, understanding these trends helps:

For investors and analysts, export shifts signal where manufacturing competitiveness and industrial policy are evolving.

Understanding export segmentation is critical because the global tire trade is not uniform. Different tire categories serve distinct markets, margin structures, regulatory environments, and growth trajectories.

Below is a detailed breakdown of the four major export segments.

Passenger car tires represent the largest share of global tire exports by volume.

Market Characteristics:

Key Export Drivers:

Competitive Dynamics:

Passenger tires are typically:

Truck and bus radial tires represent one of the fastest-growing export segments, driven by commercial transport expansion.

Market Characteristics:

Key Growth Drivers:

Competitive Landscape:

TBR tires offer:

Because logistics fleets operate continuously, demand for commercial tires remains resilient even during passenger vehicle downturns.

OTR tires serve industries such as:

Market Characteristics:

Key Growth Drivers:

Competitive Advantage:

OTR exports are:

This segment contributes disproportionately to export value compared to volume.

Aviation and industrial tires represent a niche but high-value segment of global tire trade.

Aviation Tires:

Industrial Tires:

Market Dynamics:

Countries with advanced aerospace and industrial ecosystems such as the United States, France, Germany, and Japan dominate these exports.

Strategic Implications for Importers

Diversifying sourcing strategies by segment reduces trade and supply risk.

Sustainability and ESG (Environmental, Social, and Governance) considerations are increasingly reshaping the global rubber tire export market. Buyers, regulators, and investors are placing greater emphasis on traceability, carbon impact, ethical sourcing, and circular economy practices. For exporters, ESG performance is no longer optional it is becoming a competitive differentiator.

Below is a breakdown of the key sustainability drivers influencing tire exports.

Natural rubber is a primary raw material in tire manufacturing, and most of it is sourced from tropical regions in Southeast Asia, Africa, and Latin America.

Why It Matters:

Current Export Trend:

Major tire manufacturers and exporting countries are now:

Buyers in Europe and North America increasingly require:

Exporters unable to demonstrate responsible sourcing may face restricted market access.

Tire manufacturing is energy-intensive and involves carbon-heavy inputs such as:

Export Implications:

Importing regions are increasingly evaluating:

Some exporters are responding by:

Premium buyers, particularly automotive OEMs, are now incorporating carbon footprint metrics into supplier selection.

The EU Deforestation Regulation is expected to significantly influence global rubber and tire exports.

Key Requirements:

Impact on Tire Exporters:

Exporters supplying EU markets must now demonstrate:

This is accelerating digital transformation in rubber supply chains and shifting trade advantage toward compliant exporters.

Circular economy principles are gaining traction in global tire trade.

Recycled Rubber:

Manufacturers are increasingly incorporating:

This reduces raw material dependency and lowers carbon footprint.

Retread Tires:

Retreading extends the life of commercial tires and is particularly common in:

Retread tire exports are growing due to:

Regulatory support for circular economy initiatives in Europe and North America is strengthening demand for sustainable tire solutions.

Sustainability pressures are influencing:

Exporters that demonstrate:

are more likely to secure long-term contracts with OEMs and global distributors.

From Tree to Tyre: Build a Transparent Rubber Supply Chain

Natural rubber traceability is becoming critical for global tire exports.

Read our blog on “Tree to Tyre: Building a Sustainable Rubber Supply Chain”

FSC-Certified Rubber: Turning Sustainability into Competitive Advantage

Sustainable sourcing is no longer optional — it’s a procurement requirement.

Explore our guide on Sustainable Solutions with FSC Rubber and see how certification drives long-term export resilience.

The EU Deforestation Regulation (EUDR) is reshaping rubber trade.

If you export tires to the EU, plantation-level geolocation data and due diligence documentation are mandatory.

Read our EUDR Compliance Guide for Tire Manufacturers to understand obligations, required supplier data, and how to stay audit-ready before shipments move.

While country-level export rankings provide a macro view of trade dominance, the real drivers behind global rubber tire exports are multinational tire manufacturers with extensive production networks across continents. These companies influence pricing, innovation, sustainability standards, and global supply chain strategies.

Below is a detailed overview of the leading tire manufacturers powering global exports.

Headquarters: Tokyo, Japan

Positioning: World’s largest or among the top global tire manufacturers by revenue

Strengths:

Bridgestone operates production facilities across Asia, Europe, and North America, enabling diversified export flows. The company is particularly strong in commercial vehicle and premium passenger tire segments, with significant export volumes serving global automotive manufacturers.

Headquarters: Clermont-Ferrand, France

Positioning: Premium, innovation-driven global brand

Strengths:

Michelin competes primarily in high-value segments, exporting premium tires with strong brand equity. The company is a leader in:

Michelin’s global export network spans Europe, Asia, and the Americas.

Headquarters: Akron, Ohio, USA

Positioning: Strong North American and global brand

Strengths:

Goodyear’s export strategy focuses on premium and specialty segments while leveraging regional trade agreements. It maintains production hubs across the Americas and Europe.

Headquarters: Hanover, Germany

Positioning: Technology-driven premium manufacturer

Strengths:

Continental exports premium passenger and commercial tires, with strong OEM integration across Europe. The company differentiates itself through:

Germany’s export strength in premium tires is closely tied to Continental’s global operations.

Headquarters: Milan, Italy

Positioning: High-performance and luxury segment leader

Strengths:

Pirelli focuses on high-margin segments rather than high volume. Its exports are concentrated in:

Pirelli benefits from strong brand equity and technical specialization.

Headquarters: Hangzhou, China

Positioning: Large-scale, cost-competitive global exporter

Strengths:

Zhongce Rubber (also known as ZC Rubber) is one of China’s largest tire manufacturers and a major contributor to China’s global export dominance.

The company competes primarily in:

Its global expansion strategy includes overseas manufacturing investments to mitigate trade barriers.

Headquarters: Seoul, South Korea

Positioning: Technology-forward global challenger brand

Strengths:

Hankook has grown rapidly through:

It exports heavily to Europe and North America while maintaining production bases across Asia and Europe.

These manufacturers collectively influence:

Many operate multi-country production networks, meaning:

A single company may export from China, Thailand, Germany, or the United States depending on cost structure and trade policies.

The global rubber tire trade operates within a highly interconnected and politically sensitive supply chain. While demand remains strong, exporters, importers, and distributors face multiple structural risks that can impact pricing, sourcing stability, and regulatory compliance.

Below are the five most critical risks shaping global tire trade today.

Anti-dumping duties are one of the most significant risks in the global tire export market.. Anti-dumping investigations occur when importing countries believe tires are being sold below fair market value, harming domestic producers.

Strategic Risk:

Heavy reliance on a single export market increases exposure to trade remedy actions.

Tire production depends heavily on raw materials such as:

Why It’s Risky:

The global tire industry relies on complex cross-border logistics networks.

Vulnerabilities Include:

Since tire exports are bulky and freight-intensive, transportation costs represent a significant portion of total export expenses.

Geopolitical Risk

Global tire trade is sensitive to geopolitical developments, including:

Geopolitical instability can result in:

Environmental and social governance (ESG) requirements are increasingly influencing tire exports.

Key Areas of Scrutiny:

Regulations such as deforestation and sustainability laws in major importing regions are raising compliance expectations.

TraceX helps global tire manufacturers and exporters manage sustainability, compliance, and supply chain risks by digitizing and structuring natural rubber traceability from plantation to export shipment. It enables companies to collect geolocation data, verify deforestation-free sourcing, onboard suppliers with structured KYC, and conduct automated risk assessments before raw materials enter production. By integrating with ERP and procurement systems, TraceX creates an end-to-end compliance workflow that supports ESG reporting, regulatory due diligence, and audit readiness reducing shipment delays, minimizing trade disruptions, and protecting access to regulated markets such as the EU

Between 2026 and 2030, global tire exports will be shaped by electrification, sustainability mandates, and strategic supply chain realignment. Rising EV adoption will accelerate demand for high-performance, low-rolling-resistance tires, pushing manufacturers toward advanced R&D and premium product positioning. At the same time, tightening sustainable rubber regulations, particularly in regulated markets will require deeper traceability, deforestation-free sourcing, and stronger ESG compliance frameworks. Production is likely to continue shifting toward diversified, regionally optimized manufacturing hubs to mitigate geopolitical and trade risks, while emerging exporter nations in Southeast Asia and South Asia expand capacity to capture growing demand. In this evolving landscape, competitiveness will depend not only on cost and scale, but on innovation, regulatory readiness, and resilient global supply networks.